SMM, June 5:

In 2025, the sodium-ion battery (sodium-ion battery) market is characterized by significant technological breakthroughs, cost reductions, and accelerated large-scale applications. Collaborative development across all segments of the industry chain has taken shape, with a dual-driven model of policy and market forces largely established.

In May, the sodium-ion battery market witnessed dynamic corporate activities, showcasing a thriving development momentum. On May 8, Huzhou Yingna New Energy's 10,000 mt-scale production line for composite sodium iron phosphate (NFPP) cathode materials commenced operations, marking a new phase in the commercialization of sodium-ion batteries. On May 26, Qingna Technology's 10GWh Phase I intelligent factory for large-cylinder sodium-ion batteries, themed "A New Era of Green Sodium-ion Batteries, A New Engine for Intelligent Manufacturing Industry," was successfully put into operation. As an industry leader, CATL's sodium-ion power battery for new energy passenger vehicles, released in April, has garnered significant attention. Its heavy-duty truck batteries are set to enter mass production in June, with cooperation with FAW Jiefang already in place. This initiative has greatly propelled the commercialization of sodium-ion batteries in the transportation sector, signaling their emergence in a key segment of the new energy vehicle market.

In May 2025, the sodium-ion battery industry chain demonstrated notable structural growth, with distinct differentiation in cathode materials, anode materials, electrolytes, and battery cells. Driven by both policy and market demand, upstream and downstream enterprises in the industry chain have accelerated their layouts, with capacity expansion and technological advancements progressing in tandem, injecting strong momentum into the large-scale development of the industry.

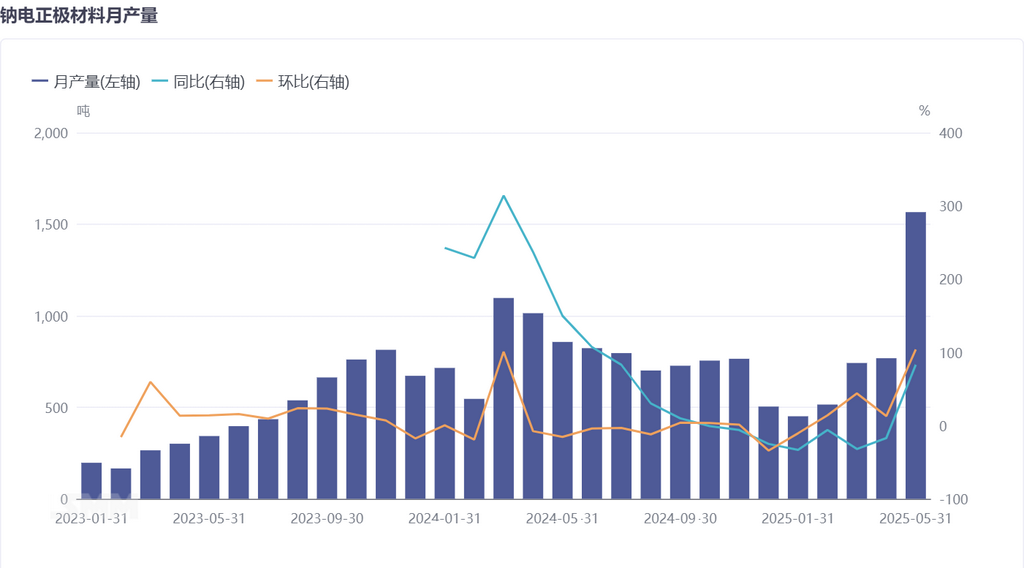

Cathode Materials: NFPP Dominance Solidified, Capacity Surges Exponentially

In May, the production of sodium-ion battery cathode materials achieved breakthrough growth, surging 104% MoM and 83% YoY. Among them, NFPP, leveraging advantages such as excellent safety performance and rapid industrialization, accounted for 73% of the total output. This achievement is attributed to the successful commissioning of multiple NFPP mass production lines over the past six months, laying a solid hardware foundation for capacity expansion. Meanwhile, downstream enterprises' recognition of NFPP has continued to rise, with a significant increase in orders, prompting some enterprises originally focused on layered oxide battery cells to gradually transition towards polyanion battery cell production, further strengthening NFPP's market dominance.

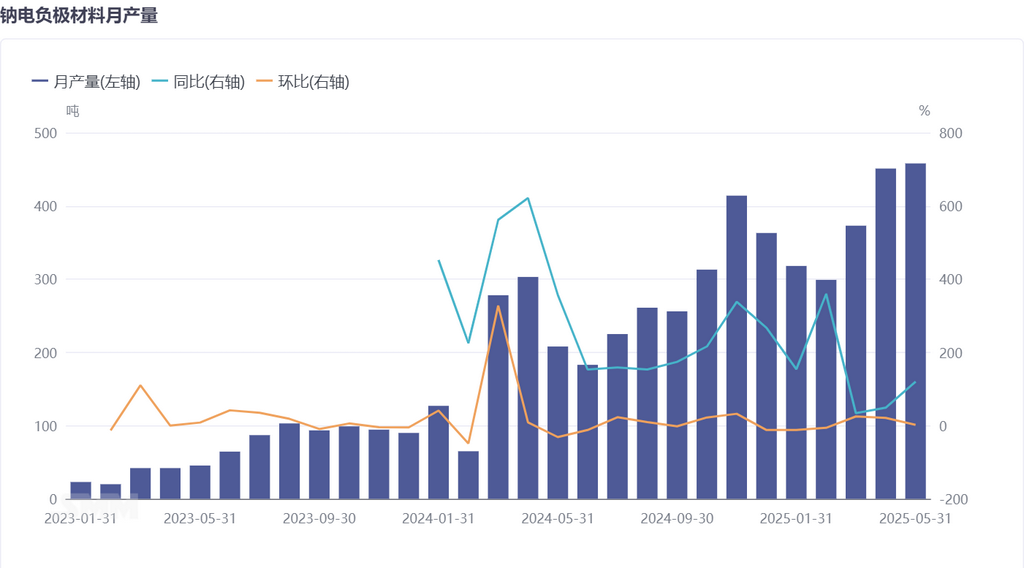

Anode Materials: Capacity Release Hindered, Growth Lags Behind

In contrast to the booming cathode materials sector, the production of sodium-ion battery anode materials in May only achieved a 2% MoM and 147% YoY increase. Currently, anode capacity has not been fully released, with multiple factors such as unstable raw material supply and difficulties in process optimization constraining the expansion of anode material production. Despite the industry's promising prospects, the anode segment still needs to overcome technological and supply chain bottlenecks in the short term to keep pace with the development of the cathode and battery cell segments.

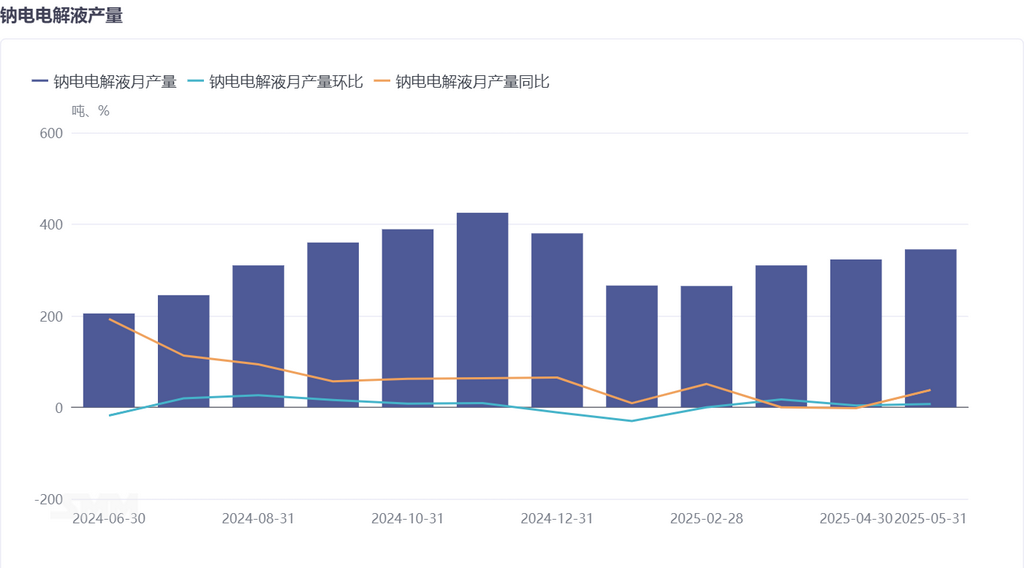

Electrolyte: Production is primarily driven by sales, with significant fluctuations in output

In May, the production of sodium-ion battery electrolytes increased by 7% MoM and 38% YoY. Due to the less stable market demand for sodium-ion batteries compared to lithium batteries, electrolyte companies generally adopt a "produce based on sales" model. Additionally, the stringent environmental requirements for electrolyte storage keep corporate inventory levels low, resulting in production being highly dependent on orders received in the current month. This production characteristic leads to greater volatility in the electrolyte segment of the industry chain.

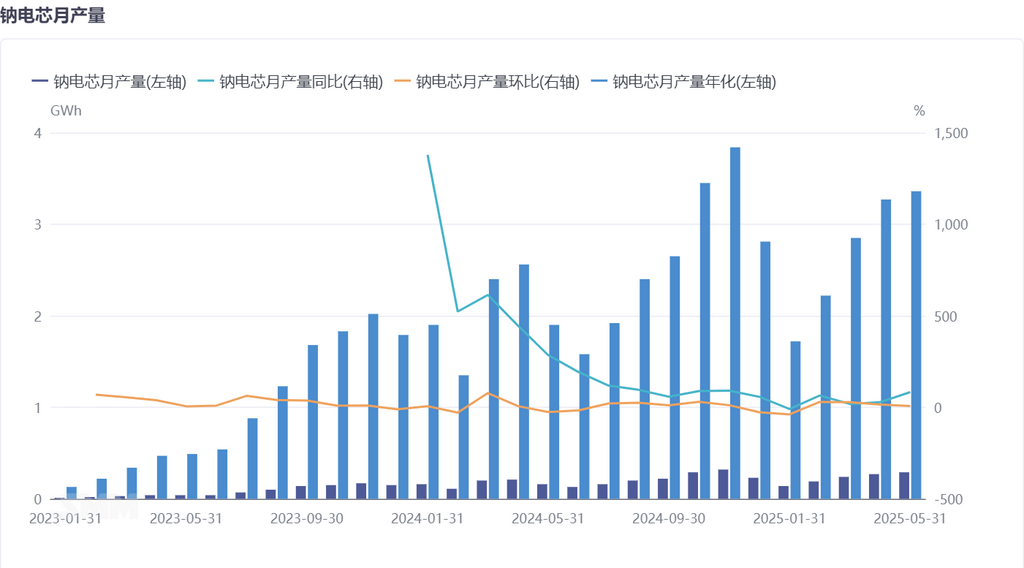

Battery Cell: Demand expectations are positive, with significant potential for production growth

In May, the production of sodium-ion battery cells increased by 7% MoM and 83% YoY. With the concentrated launch of multiple sodium-ion ESS projects in H2, the rising penetration of sodium-ion batteries in electric two-wheelers, and the growth in demand for start-stop power supplies, the battery cell segment is expected to experience a new round of explosive growth. Companies are actively expanding production and stockpiling inventory, anticipating that battery cell production will continue to rise in the coming months, accelerating the commercialization of sodium-ion batteries in multiple fields.

In May 2025, various segments of the sodium-ion battery industry chain exhibited uneven development trends. Cathode materials led the industry with technological and capacity advantages, with NFPP becoming the core growth engine. Anode materials faced capacity release delays due to raw material and technological bottlenecks. Electrolytes demonstrated a "produce based on sales" characteristic due to demand fluctuations. The battery cell segment, however, benefited from the expansion of downstream application scenarios, showing significant growth potential. Overall, despite the varying development paces of each segment, the sodium-ion battery industry is accelerating towards large-scale production, and its market potential in fields such as ESS and transportation is promising.

SMM New Energy Research Team

Wang Cong 021-51666838

Ma Rui 021-51595780

Feng Disheng 021-51666714

Lv Yanlin 021-20707875